Whether you are new to capital markets or looking to refresh your technical knowledge, this primer breaks down the essentials of modern securities lending. We will explore the foundational mechanics of the trade, examine how past market turbulence shaped today's safeguards, and unpack how this critical market function connects to pressing regulatory requirements.

Motivation

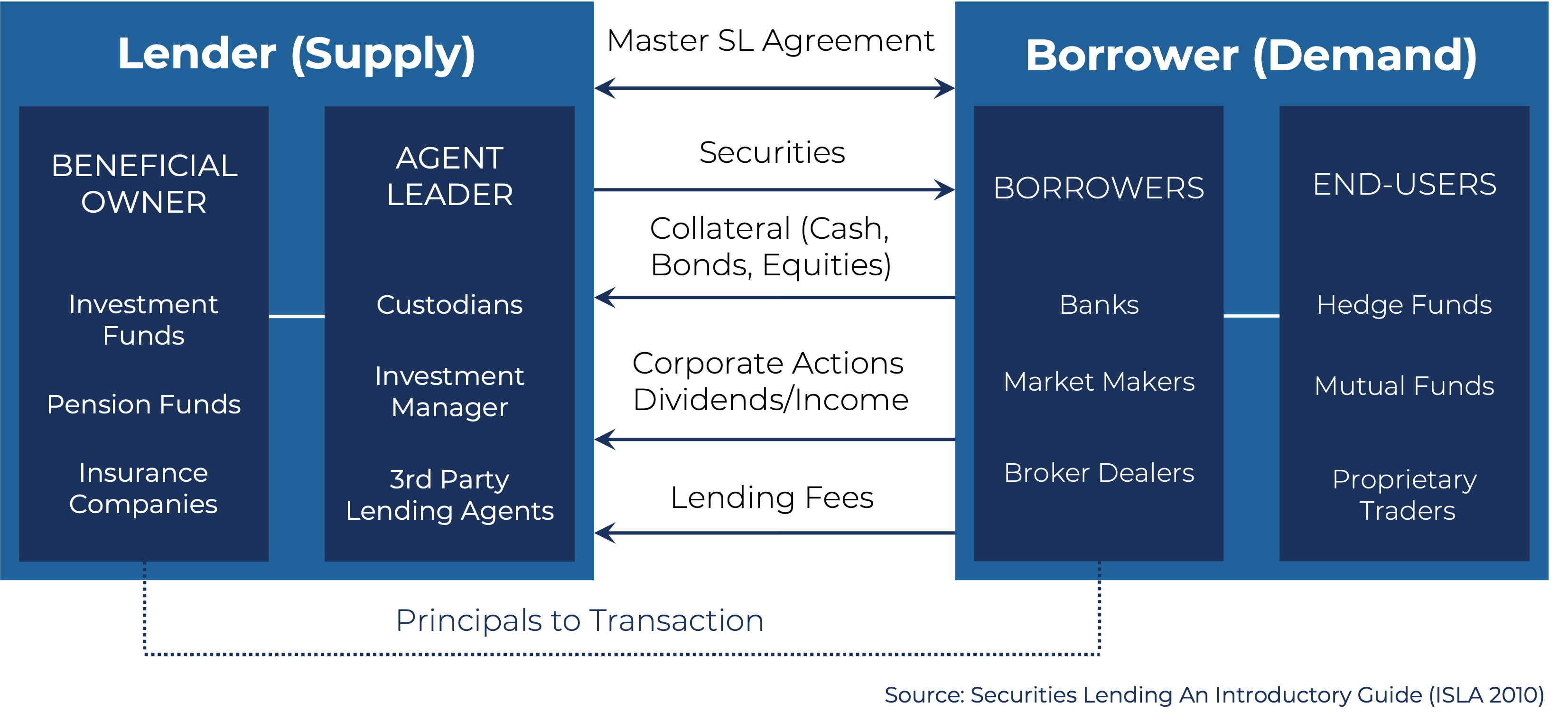

Securities lending fulfills several important functions in a healthy capital market. It makes financial markets more liquid, provides a low-risk means for investors to generate additional portfolio income, and, crucially, reduces operational risk in the system.

At its core, securities lending and borrowing is a contract agreed by two parties, where an investor temporarily lends securities to a borrower, in return for a fee. Along with repurchase transactions (repos), buy-sell back transactions, and margin or commodity lending, it forms one of the four different securities financing transaction (SFT) types.

The Role of ISLA and the GMSLA in Global Markets

International Securities Lending Association (ISLA) is a leading industry trade body dedicated to promoting safe and efficient capital markets. To facilitate seamless cross-border transactions, ISLA publishes the most widely adopted standard contract for the industry: the Global Master Securities Lending Agreement (GMSLA).

The GMSLA provides a comprehensive and robust set of rules governing the relationship between the lender and the borrower. It establishes clear protocols for critical operational mechanics, including the transfer and valuation of collateral, the handling of corporate actions and manufactured dividends, margin maintenance, and default procedures. By establishing this common legal baseline, the GMSLA minimizes counterparty friction and allows financial institutions to execute complex international lending activities with clarity and confidence.

Important Concepts

1. The Foundation: Title Transfer & Economic Ownership

In securities lending, most transactions are carried out using an "outright transfer of title". This means that the absolute legal title to both the loaned securities and the provided collateral passes completely to the borrower and the lender, respectively, free of any encumbrances. However, even though the borrower holds the legal title during the transaction, the economic ownership—meaning the financial benefits attached to those securities—remains with the original lender.

2. Risk Mitigation: Margin & Collateral ManagementTo protect the lender from the risk of the borrower defaulting, the borrower must provide collateral simultaneously with the delivery of the loaned securities. Moreover, lenders often limit the borrowers (counterparties) to approved, creditworthy entities. Concentration limits are frequently imposed, such as not lending more than a specific percentage of a portfolio to a single borrower or not lending more than 50% of the aggregate market holding of a specific issue.

Margin: The market value of this collateral must equal the market value of the loaned securities plus an agreed-upon additional percentage, known as the "Margin".

Mark-to-Market:Because market prices fluctuate during the life of the loan, the securities and collateral are marked to market, usually on a daily basis. If the collateral value falls below the required threshold, the lender has the right to demand further collateral. Conversely, if it exceeds the threshold, the borrower has the right to call for the return of the excess collateral.

3. During the Trade: Income Payments, Corporate Actions & VotingThe general principle is that the lender should be treated as if they had never lent out the security in the first place. Because the borrower holds the legal title, they receive all dividends or interest coupons paid by the issuer during the life of the loan.

Manufactured Payments: The borrower must pass any financial benefits (for example received dividends) back to the lender as a "manufactured payment". Specifically, the borrower must pay a sum of money or deliver property equivalent to the type and amount of income the lender would have received had they retained the securities. Conversely, any financial benefits earned by the collateral shall be returned to the original owner (the borrower, in this case).

Corporate Actions: If a corporate action (such as a rights issue or a takeover offer) occurs, the lender can require the borrower to redeliver equivalent securities in the specific form that results from exercising that corporate action, provided the lender gives notice in good time.

Voting Rights: The borrower has no obligation to exercise voting rights on the loaned securities according to the lender's instructions. Furthermore, to align with best practices, the GMSLA requires the borrower to explicitly warrant that they are not entering into the loan for the primary purpose of obtaining or exercising voting rights.

4. Events of Default & NettingThe GMSLA strictly defines "Events of Default," which include acts of insolvency, failure to pay cash collateral, or a breach of warranty. If a default occurs, both parties' payment and delivery obligations are immediately accelerated. The non-defaulting party determines the "Default Market Value" of the owed securities. Through a process of set-off (close-out netting), all mutual obligations are calculated against each other, and only the net balance is payable by one party to the other on the next business day.

Evolution of the GMSLA (2000 to 2010)

The updated 2010 GMSLA includes more robust protections resulting from the lessons learned during the 2007-2008 financial crisis. By updating the core concepts detailed above, the new framework promotes better stability in illiquid and turbulent market conditions. Key changes include:

Flexible Default Valuations: The 2010 agreement introduced more flexible "Net Value" default valuations for illiquid securities if standard market quotes are not commercially reasonable or available.

Mini Close-Outs: A failure to deliver equivalent securities or non-cash collateral is no longer categorized as an event of default. Instead, it triggers a "mini close-out" mechanism, which allows the non-defaulting party to terminate only the affected loan rather than accelerating all outstanding obligations across the board.

Grace Periods: A three-day grace period was introduced for a failure to make a manufactured payment before it can be declared an event of default.

Regulatory Evolution and Market Integrity

Securities lending is a vital mechanism that ensures liquidity and efficiency in global capital markets. However, the historical complexity of cross-border tax regimes occasionally led to structural vulnerabilities. In the past, practices surrounding dividend arbitrage—commonly referred to in public discourse as Cum-Ex or Cum-Cum transactions—highlighted the challenges of misaligned, multi-jurisdictional tax laws.

Over the past decade, both regulators and the financial industry have undergone a significant evolution to harmonize these frameworks. Today, robust regulatory protections are in place to ensure market integrity and prevent the exploitation of tax differentials. For instance, as a standard de-risking practice, financial institutions now routinely recall loaned equities—or restrict new lending entirely—surrounding dividend record dates. This proactive measure ensures that trading activities remain unequivocally aligned with their underlying economic purpose, avoiding even the appearance of tax-motivated arbitrage.

A cornerstone of this modern compliance landscape is the Directive on Administrative Cooperation 6 (DAC 6). By requiring intermediaries to proactively disclose specific cross-border transaction "hallmarks," DAC 6 provides enhanced transparency. This framework fosters a collaborative environment between financial institutions and tax authorities, functioning as an early-warning system that aligns cross-border trades with their intended economic purpose and ensures ongoing, robust compliance across the sector.

Importance of Correct Implementation: FRTB and Capital Requirements

Securities lending and borrowing is vital for the ability of EU financial institutions to meet their risk management regulatory capital requirements, thereby reducing systemic risk. EU legislation requires banks and other market participants to reduce risk by 'collateralising' their exposures.

When correctly implemented, securities lending enables institutions to meet the Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio requirements under the Capital Requirements/Basel framework, which mandate that banks hold high-quality liquid assets. As the international Basel framework considers minimum haircuts for non-centrally cleared SFTs, proper implementation and reporting are critical to guard against regulatory arbitrage and limit the build-up of excessive leverage outside the banking system.

Conclusion and Outlook

Looking ahead, the securities lending market is set to play an increasingly pivotal role in boosting the competitiveness and liquidity of global capital markets. In Europe, there is significant untapped potential in the securities supply held within the portfolios of EU-based lenders, such as pension funds, insurance companies, and UCITS.

To fully unlock this potential and meet growing funding demands, the industry is advancing toward greater infrastructure efficiency and digitisation. The adoption of standardized frameworks, such as the FINOS Common Domain Model (CDM), aims to create a single data standard representing securities lending, repo, and derivative transactions. This will improve interoperability, streamline post-trade activities, and significantly reduce operational costs. Furthermore, as settlement cycles accelerate (such as the move to T+1) and penalty regimes like the Central Securities Depositories Regulation (CSDR) mature, securities borrowing will remain the primary operational tool to prevent settlement fails and ensure a frictionless, highly liquid market.